The Financial Iceberg Beneath the High-Mix Manufacturing Floor

The Food & Beverage (F&B) sector presents one of the most operationally complex challenges in manufacturing. Unlike durable goods, F&B operations are a relentless race against time, regulated by stringent safety protocols, often dealing with perishable inventory, and dictated by volatile consumer demand—from seasonal spikes in ice cream production to daily fluctuations in ready-meal fulfillment.

This inherent volatility masks a critical financial gap: the disconnect between the operational metrics (yield, OEE, downtime, scrap) and the C-suite’s language of liquidity, working capital, and shareholder return. When a multi-site F&B business faces distress—be it margin compression, a failed digital rollout, or integration issues following an acquisition—the need arises for a specialized profile: the Turnaround Consultant who is fluent in both the intricate science of food processing and the rigorous logic of advanced financial modeling.

If your leadership team or investors are seeking a multi-plant restructuring, they are not looking for a “deck-only consultant.” They require a leader capable of executing a diagnosis on the plant floor, designing a Lean restructuring plan, and—crucially—building and owning the integrated 13-week cash flow and 3-statement pro-forma model that justifies and tracks the transformation. This is the ultimate test of Operational Excellence.

The Operational Imperatives in Food Manufacturing

A successful F&B turnaround begins by attacking the waste streams unique to the sector. While traditional manufacturing fights the 7 Wastes (Muda), F&B adds layers of complexity related to freshness, temperature, and regulatory compliance. The consultant must address these three core operational imperatives and quantify their financial impact:

1. Perishable Inventory and Working Capital Release

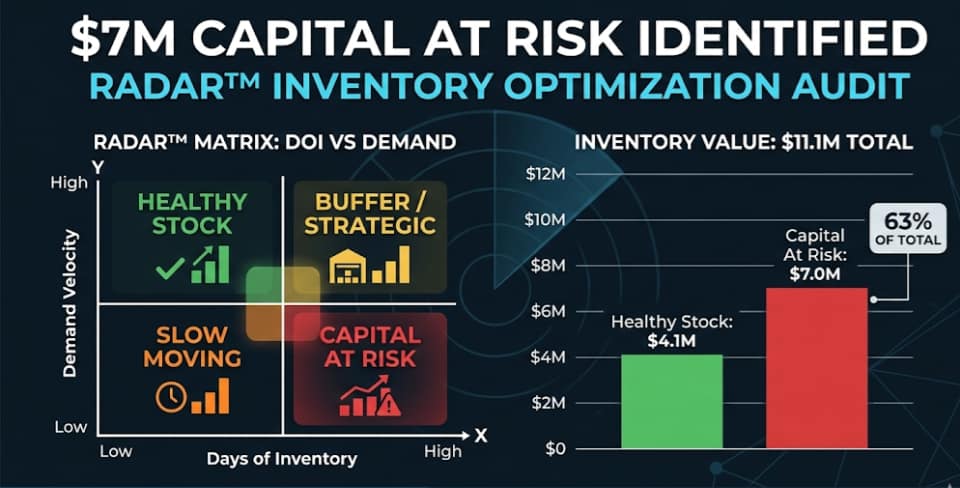

In F&B, inventory is not just money sitting idle; it’s money actively spoiling. Reducing inventory holding times (days inventory outstanding, or DIO) is the fastest way to release working capital and improve liquidity. This requires immediate action on the factory floor to synchronize supply and demand and implement FIFO practices rigorously.

The Turnaround Consultant must be able to calculate the precise dollar value of spoilage reduction (yield improvement) and translate that into reduced Cost of Goods Sold (COGS) in the Income Statement, reduced inventory on the Balance Sheet, and, ultimately, a direct positive impact on the 13-week cash flow model’s weekly liquidity forecast. Without this financial link, Lean efforts are perceived as mere “cost cutting” rather than strategic working capital management.

2. High-Mix Production and Changeover Efficiency

F&B is characterized by high-mix production driven by flavor variants, packaging sizes, and seasonal promotions. This leads to excessive and prolonged equipment changeovers, which slash Overall Equipment Effectiveness (OEE) and erode capacity. The effective consultant implements methodologies like SMED (Single Minute Exchange of Dies) to drastically reduce changeover times.

A mere 15-minute reduction in changeover time on a high-volume line might allow for an entire extra batch run per shift. The consultant must model this capacity gain to demonstrate the financial upside: increased throughput, higher machine utilization, and a reduction in the need for costly overtime labor—all of which feed directly into the pro-forma Income Statement and the Capex strategy (by proving current assets can handle higher volume).

3. Multi-Site Consolidation and Cold Chain Logistics

The job description often requires experience with multi-plant consolidation—an intense exercise in complexity, especially when dealing with cold chain logistics. When consolidating two food processing plants, the integration of distinct production lines, labor agreements, and disparate ERP/WMS systems must be managed without disrupting the supply of perishable goods.

The operations leader must model scenarios for plant footprint reduction, calculating:

- The one-time cash disbursements for equipment relocation and severance (impacting the 13-week cash flow immediately).

- The long-term savings from reduced lease costs and overhead absorption (impacting the 3-statement model).

- The change in freight costs (logistics modeling) due to the new distribution network.

This requires boots-on-the-ground knowledge of layout design (Industrial Engineering) combined with the ability to quantify the financial benefit of reduced overhead and optimized logistics networks.

The Financial Mandate: Why Modeling Cannot Be Delegated

The difference between an effective operations leader in a turnaround and a typical operations manager lies in the mastery of integrated financial forecasting. The consultant must personally own the financial models because the operational levers are the models’ core inputs.

1. The 13-Week Cash Flow: This direct-method model is the lifeline of a distressed F&B company. Every operational decision—speeding up inventory turns, delaying a non-critical vendor payment, improving yield—must be tested against the weekly liquidity forecast. The consultant must tie throughput improvements (higher sales receipts) and inventory reduction (lower disbursements for raw material) directly into this model.

2. The Integrated 3-Statement Model: This pro-forma model is the future blueprint. The consultant must define the operational assumptions—e.g., “Yield increases from 95% to 98% in Q3,” “Total labor hours reduced by 15% after consolidation,” “OEE improves from 65% to 75%”—and show how these changes flow, in an integrated manner, through the Income Statement (higher Gross Margin), Balance Sheet (lower Inventory/Fixed Assets), and Cash Flow Statement.

The UPKAIZEN Difference: Execution Over Advisement

The market is clear: the most valued consultants are the ones who do the analysis and then go to the factory floor to fix it. At UPKAIZEN, our training and consulting programs are designed to bridge this exact gap. We equip leaders with the advanced knowledge of Lean, Six Sigma, and TOC, combined with the rigorous financial quantification necessary to deliver tangible, measurable ROI directly to the P&L and Balance Sheet.

For complex F&B operations, simply knowing the tools is not enough; one must know how to integrate these tools into a solvent financial strategy. This is the definition of Operational Excellence at the C-Suite level.

Conclusion: Bridging the Gap from Strategy to Liquidity

The turnaround environment in the Food & Beverage sector demands leaders who are not merely experts in Lean tools, but professionals capable of executing a financial strategy. The low OEE, the high scrap rates, and the inventory churn—these are all financial symptoms, not just operational glitches.

The true measure of success for any multi-plant restructuring is the rapid, sustained, and auditable improvement across the entire cash conversion cycle. By mastering the integration of operational excellence methodologies with advanced financial modeling (13-week cash flow and 3-statement pro-formas), a leader transforms from an advisor into a solver.

At UPKAIZEN, we commit to building this rare breed of leadership. Stop commissioning “deck-only” advice and start driving measurable financial results from the factory floor. The time for execution is now. Invest in the skills that directly impact your P&L and liquidity.

Ready to implement Lean in your food production facility?

Contact UPKAIZEN for a tailored consultation.

Subscribe To Our Newsletter

Join our community of like-minded Operational Excellence enthusiasts and subscribe to our newsletter for the latest trends, expert insights, and exclusive content delivered straight to your inbox. Let’s connect, explore and discover excellence in every step.